A hot topic in the EV world lately has been a reported “price war” controversy in China, and perhaps extending a bit beyond that. Some automakers have contended that BYD is engaged in an extreme, destructive price war. We’ve seen various takes on this from different automakers, and China’s Ministry of Industry and Information Technology (MIIT) even got involved, convening a meeting of key automakers engaged in this matter.

One of the things that’s been implied is that BYD — and then others — can’t be making money on their EVs at the price levels they’ve gotten down to. One issue with that argument is that this price cutting and earlier accusations of artificial price wars go back years, and yet those price cuts two or three or four years ago were sustainable, weren’t financially crushing, and turned out quite well when it comes to growing EV sales and expanding EV market share. Another issue with it is something a reader pointed out — BYD’s making money on its cars.

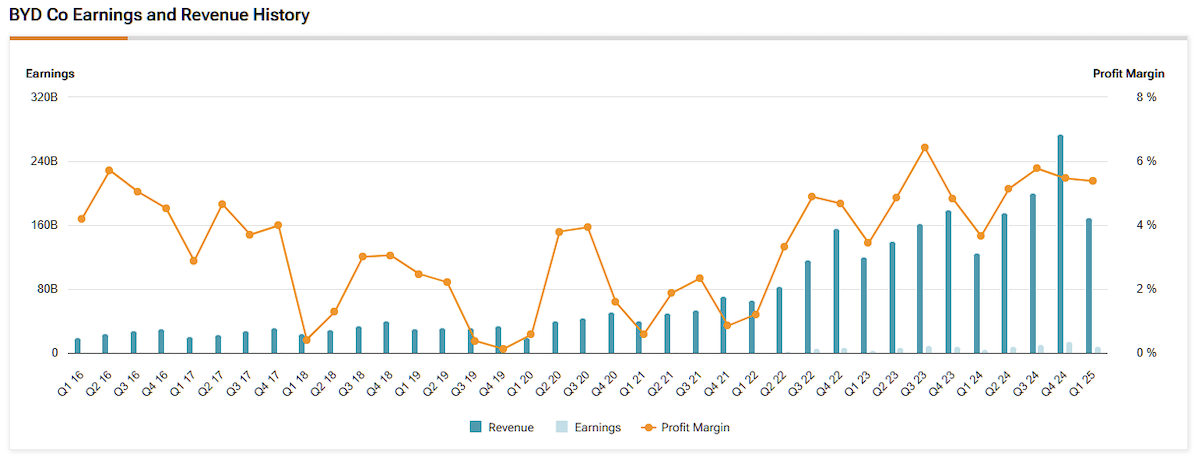

In particular, he shared the following graph showing that BYD’s profit margin (above 5%) was better in Q1 2025 than in most quarters in the past decade. There are just a few quarters that were even notably higher.

So, yes, BYD may be cutting EV prices over and over again, but it’s also making profits, so what’s the reason it shouldn’t be cutting prices? If the company can cut production costs and then pass those cuts on to buyers with price cuts, why shouldn’t it?

“In China, Li Auto and Geely also turn a profit on EVs. Xiaomi has positive gross margin on their automotive business and anticipate positive net on automotive in 2H (somewhat easier than other automakers to predict, as the product offering is limited and vehicles are sold out through the end of the year). Some others are closing the gap…

“And BYD only has ~15% of the overall automotive market in China. They are well ahead in overall sales, intelligent driving vehicles, NEVs, BEVs and PHEVs, but their share of the overall Chinese market is less than GM’s share of the US market now (and GM historically had a majority share in US for decades). China is still the most competitive automotive market in the world. BYD could double sales and still have a smaller share of the overall Chinese market than VW has in Germany. Still not be close to triggering Chinese anti-monopoly measures.

“However, companies who are consistently selling at a loss distort the market. The game becomes more about attracting capital than about solving for customer needs. (It isn’t just China, look a Lucid’s losses per vehicle and new advertised price cuts). Companies that were never in a position to turn a profit will deepen losses. Profitable automakers will have challenges to their business models. Bringing prices in line so that competitor costs to come closer to breaking even will make the overall market healthier. I have a feeling that some regulations might be coming to prevent automakers in China from selling below COGS (negative gross margin), even if the company overall posts a net loss.

“On BYD specifically, it is important to remember that they didn’t just reach profitability. While net margins have fluctuated, they have remained positive as their business evolved. It goes farther back than the chart below. Most of their startup competitors fueled growth by attracting capital to fund years of losses. Tesla didn’t turn their first full year of net profitability until 2020, halfway through this chart. BYD has stayed net profitable and grown gross margins to reinvest in R&D and business growth. Typically, when net profits have risen, they reinvest, increase R&D and/or cut prices to increase scale. From a historical perspective, current net margins are relatively high and overall earnings are growing, so I would expect them to make some shifts.”

When your R&D “team” is brilliant, and has more people working in it than most automakers have employees overall, you reap the benefits. Perhaps the big price cuts are just a result of ongoing incremental improvements. For any automakers that can’t hang, perhaps it’s just that they don’t have the advantages BYD now has.

Larry went on:

“If you look at the fine print of the BYD ‘price cuts,’ relatively few people will get the advertised price that has caused such a fervor. The listed price includes the government scrappage incentive (up to $2700 to scrap an ICE vehicle over a decade old) and the BYD trade-in subsidy (to get the maximum of that, you need an old BYD). BYD never sold that many ICE vehicles and many have already been scrapped. On cars like the Seagull, the promotion is basically just the government scrappage subsidy. On some of the other models with the larger incentives, they tend to be older and facing increased internal competition from new models. Overall, it makes sense to sweeten the scrappage program, as it takes ICE cars off the road that no longer fit BYDs business and involve expenses around stocking parts.

“With few people likely to get the full amount advertised, and I expect BYD to post another quarter of solid financials. 1Q had a lot of expenses from launching dozens of new and refreshed models and the seasonal sales dip, while the launches have slowed in 2Q and volume is seasonably up from the previous quarter.

“Overall, I feel like too many of BYD’s competitors are focused on trying to ‘beat’ them, rather than focusing on improving their business, overtaking ICE and expanding globally.”